BKM04AC(A) Financial Analysis

Question 1: Introduction/framework

A. (5p.) The answer must address the following issues (partial credit can be awarded):

- Accounting rules that are aimed at reducing earnings management typically reduce management’s

accounting flexibility/discretion (i.e., these rules are more rigid)

- Consequently, management has less opportunity to make accounting choices that make financial

statements informative (about the firm’s economic performance) [or, alternatively stated: management

has less opportunity to communicate its private information in the financial statements]

B. (5p.) The answer must address the following issues (partial credit can be awarded):

- The lemons problem implies that investors cannot distinguish between good and bad business ideas or

high-quality/low-quality firms, driving up the high-quality firm’s cost of capital

- To reduce their cost of capital, high-quality firms have an incentive to reduce the information

asymmetry between management and investors (using voluntary disclosure)

Question 2: Accounting analysis

A. (4p.) Please check pages 97-98 of the book for a list of incentives.

B. (4p.)

Allowance at beginning of year (new) = 25% x 100,000 = 25,000

Allowance at end of year (new) = 25% x 80,000 = 20,000

Bad debt expense (new) = 20,000 – 25,000 + 5,000 (write-offs) = 0

Given: Bad debt expense (old) = 2,000

Adjustments: Decrease bad debt expense (-2,000); Increase tax expense (30% x 2,000 = 600); decrease net

profit (-2,000 + 600 = -1,400)

C. (5p.)

Net debt and net asset adjustment at the beginning of 2011: + €500 million

Equity adjustment at the beginning of 2011: 0 million

Net debt (old) = 0.55 x 3,400 = 1,870 million; net debt (new) = 1,870 + 500 = 2,370 million

Net debt to net capital (new) = 2,370 / (3,400 + 500) = 0.608 (versus 0.55 (old))

Lease expense (old) = €80 million

Lease expense (new) = depreciation expense + interest expense = 500/5 + 10% x 500 = 150 million

Net profit (old) = 0.10 x (3,400 – 1,870) = 153

Net profit (new) = 153 + (80 - 150) x (1 – 0.3) = 104 million

ROE (new) = 104/(3,400 – 1,870) = 0.068 (versus 0.10 (old))

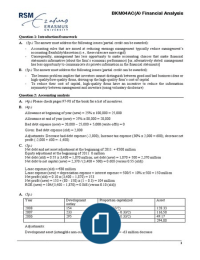

A. (5p.)

Year Development Proportion capitalized Asset

outlay

2008 154 X (1 – 0.33/2) 128.33

2007 233 X (1 – 0.33 – 0.33/2) 116,50

2006 295 X (1 – 0.67 – 0.33/2) 49.17

294,00

Adjustments:

Development asset (intangible non-current assets): (294 – 357) = -63 million decrease

__________________________________________________________________________________________________

1

Question 1: Introduction/framework

A. (5p.) The answer must address the following issues (partial credit can be awarded):

- Accounting rules that are aimed at reducing earnings management typically reduce management’s

accounting flexibility/discretion (i.e., these rules are more rigid)

- Consequently, management has less opportunity to make accounting choices that make financial

statements informative (about the firm’s economic performance) [or, alternatively stated: management

has less opportunity to communicate its private information in the financial statements]

B. (5p.) The answer must address the following issues (partial credit can be awarded):

- The lemons problem implies that investors cannot distinguish between good and bad business ideas or

high-quality/low-quality firms, driving up the high-quality firm’s cost of capital

- To reduce their cost of capital, high-quality firms have an incentive to reduce the information

asymmetry between management and investors (using voluntary disclosure)

Question 2: Accounting analysis

A. (4p.) Please check pages 97-98 of the book for a list of incentives.

B. (4p.)

Allowance at beginning of year (new) = 25% x 100,000 = 25,000

Allowance at end of year (new) = 25% x 80,000 = 20,000

Bad debt expense (new) = 20,000 – 25,000 + 5,000 (write-offs) = 0

Given: Bad debt expense (old) = 2,000

Adjustments: Decrease bad debt expense (-2,000); Increase tax expense (30% x 2,000 = 600); decrease net

profit (-2,000 + 600 = -1,400)

C. (5p.)

Net debt and net asset adjustment at the beginning of 2011: + €500 million

Equity adjustment at the beginning of 2011: 0 million

Net debt (old) = 0.55 x 3,400 = 1,870 million; net debt (new) = 1,870 + 500 = 2,370 million

Net debt to net capital (new) = 2,370 / (3,400 + 500) = 0.608 (versus 0.55 (old))

Lease expense (old) = €80 million

Lease expense (new) = depreciation expense + interest expense = 500/5 + 10% x 500 = 150 million

Net profit (old) = 0.10 x (3,400 – 1,870) = 153

Net profit (new) = 153 + (80 - 150) x (1 – 0.3) = 104 million

ROE (new) = 104/(3,400 – 1,870) = 0.068 (versus 0.10 (old))

A. (5p.)

Year Development Proportion capitalized Asset

outlay

2008 154 X (1 – 0.33/2) 128.33

2007 233 X (1 – 0.33 – 0.33/2) 116,50

2006 295 X (1 – 0.67 – 0.33/2) 49.17

294,00

Adjustments:

Development asset (intangible non-current assets): (294 – 357) = -63 million decrease

__________________________________________________________________________________________________

1