Flexible Budgets, Direct-Cost Variances

A variance is the difference between actual results and

expected performance. The expected performance is also

called budgeted performance, which is a point of reference

for making comparisons.

Management by exception is a practice whereby managers

focus more closely on areas that are not operating as

expected and less closely on areas that are.

Understand the reason for the decrease (better operator

training or changes in manufacturing methods) so these

practices can be continued and implemented by other

divisions

Evaluating performance to motivate manager

Variances help to make more informed predictions

about the future and thereby improve the quality of the

A flexible budget calculates budgeted revenues and

five-step decision making process

budgeted costs based on the actual output in the budget

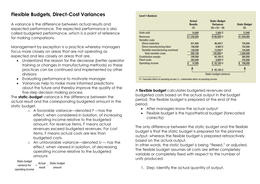

The static-budget variance is the difference between the

period. The flexible budget is prepared at the end of the

actual result and the corresponding budgeted amount in the

period.

static budget.

After managers know the actual output

o A favorable variance—denoted F —has the

Flexible budget is the hypothetical budget (forecasted

effect, when considered in isolation, of increasing

correctly)

operating income relative to the budgeted

amount. For revenue items, F means actual

The only difference between the static budget and the flexible

revenues exceed budgeted revenues. For cost

budget is that the static budget is prepared for the planned

items, F means actual costs are less than

output, whereas the flexible budget is prepared retroactively

budgeted costs.

based on the actual output.

o An unfavorable variance—denoted U — has the

In other words, the static budget is being “flexed,” or adjusted.

effect, when viewed in isolation, of decreasing

The flexible budget assumes all costs are either completely

operating income relative to the budgeted

variable or completely fixed with respect to the number of

amount

units produced.

1. Step: Identify the actual quantity of output.

A variance is the difference between actual results and

expected performance. The expected performance is also

called budgeted performance, which is a point of reference

for making comparisons.

Management by exception is a practice whereby managers

focus more closely on areas that are not operating as

expected and less closely on areas that are.

Understand the reason for the decrease (better operator

training or changes in manufacturing methods) so these

practices can be continued and implemented by other

divisions

Evaluating performance to motivate manager

Variances help to make more informed predictions

about the future and thereby improve the quality of the

A flexible budget calculates budgeted revenues and

five-step decision making process

budgeted costs based on the actual output in the budget

The static-budget variance is the difference between the

period. The flexible budget is prepared at the end of the

actual result and the corresponding budgeted amount in the

period.

static budget.

After managers know the actual output

o A favorable variance—denoted F —has the

Flexible budget is the hypothetical budget (forecasted

effect, when considered in isolation, of increasing

correctly)

operating income relative to the budgeted

amount. For revenue items, F means actual

The only difference between the static budget and the flexible

revenues exceed budgeted revenues. For cost

budget is that the static budget is prepared for the planned

items, F means actual costs are less than

output, whereas the flexible budget is prepared retroactively

budgeted costs.

based on the actual output.

o An unfavorable variance—denoted U — has the

In other words, the static budget is being “flexed,” or adjusted.

effect, when viewed in isolation, of decreasing

The flexible budget assumes all costs are either completely

operating income relative to the budgeted

variable or completely fixed with respect to the number of

amount

units produced.

1. Step: Identify the actual quantity of output.